The Marketplace

Commercial Real Estate Trends

2021 Commercial Real Estate Industry Outlook

Article posted on Dec 3, 2020 to Deloitte.com/us

Written by Jim Berry and Kathy Feucht on Deloitte's outlook for 2021 Commercial Real Estate

Breaking inertia, gaining momentum

THE impact of COVID-19 on the global economy and the CRE industry has made 2020 the most memorable year in recent history. CRE companies have needed to digitize operations, close physical facilities due to extensive lockdowns, and prepare for reopening, while ensuring the health and safety of employees and occupiers and considering the financial health of tenants and end users.

With economic recovery heavily dependent on a vaccine, the length of this downturn remains uncertain. As we write this outlook, economic activity is contracting due to a fresh resurgence of the virus in Europe.1 Large Asia-Pacific (APAC) economies such as Japan and Australia haven't yet turned the corner to growth, India is facing a severe downturn, and strained relationships between the United States and China are creating significant geopolitical tensions.2 According to Deloitte's economic forecast, in the United States, it is expected that "a vaccine and/or treatment will allow normal economic activity to begin to resume in mid-2021."3 As it will take time to deploy the vaccine, our economists expect growth to remain somewhat constrained for a period of time.4 (Click here to read Deloitte's latest US Economic Forecast.)

The CRE macro environment is being impacted similarly. But there is a dichotomy in operating fundamentals among property types-industrial real estate, health care, data centers, and cell towers have been positively disrupted, while offices, hotels, and retail have felt the negative effects. Global CRE deal volume declined 36% year over year (YoY) to US$306B in 2Q20 due to economic stagnation and an uncertain pricing environment.5 Prices are showing early signs of stress across the more negatively impacted property types. 6 For instance, US retail and office price indices declined 4.1% and 0.5% YoY in August. In contrast, industrial property index rose 7.4% YoY.7 Unlike the Global Financial Crisis (GFC), CRE companies had generally strong financials at the start of the pandemic and debt markets remain sufficiently liquid. Yet, troubled loans are rising; banks, fearing higher delinquencies, are tightening lending standards.8 In several sectors, rent collections have remained healthy, but largely because of higher tenant incentives and leasing concessions. Along with the evolving financial landscape, the pandemic has resulted in tectonic shifts in the way people live, work, and play, which has put unique pressures on certain property sectors.

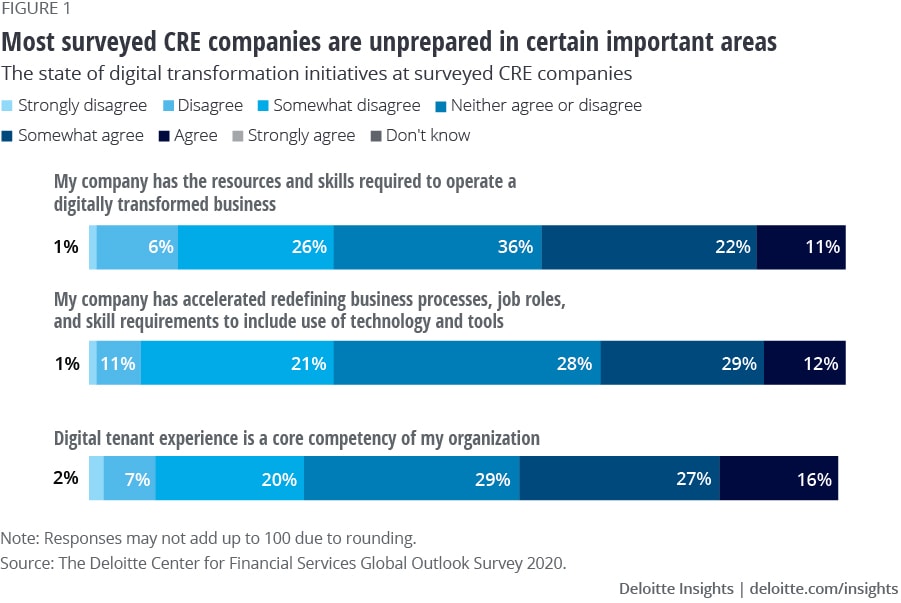

With this as the backdrop, we wanted to understand how well-equipped CRE leaders were to weather the current economic situation, how they are planning to recover over the next 12 months, and how they are preparing to remain competitive and thrive in the long term. To do this, we surveyed 200 CRE senior executives-owners/operators, developers, brokers, and investors-in 10 countries during the summer of 2020. (See sidebar, "Methodology," for more details about the survey.) Overall, most survey respondents felt their companies were unprepared in certain important areas and that the industry continues to struggle to adapt their long-term strategies (figure 1). Some key challenges:

- Only one-third of respondents agree or strongly agree that they have the resources and skills required to operate a digitally transformed business.

- Less than 50% of respondents consider digital tenant experience a core competency of their organization.

- Only 41% of respondents said their company has stepped up efforts to redefine business processes, job roles, and skill requirements to include the use of technology and tools.

CRE company leaders have their work cut out. To position their companies to thrive long term, they need to break inertia to move into rapid recovery. As monumental as 2020 has been, 2021 could be even more so; the critical decisions and investments leaders make now could come to fruition over the next 12 months. They should strive to be digital-optimizing business, operating, and customer models for a digital environment. Rapid digital transformation will likely be needed to build operational resilience, maintain a strong financial position, develop and retain talent, and create an enabling culture.

Mastering the tightrope

For many CRE industry leaders, the pandemic has been an eye-opener. It has tested the resilience of every single leader across the globe, and likely will for many months to come.

COVID-19 has forced companies to focus on cost containment and for many, heightened the need for-and pace of-digital transformation. Yet, the importance of empathy and human connection is also coming to the fore. People are increasingly missing human interaction, which was vastly reduced or eliminated due to shelter-in-place orders for a long period of time, and in some regions continues. And people remain anxious about their health and well-being and the health and well-being of their families and friends, which is compounded by growing concerns about climate change and political unrest in many parts of the world.37

Leaders should therefore master the art of walking on a tightrope-balancing business recovery, seizing new opportunities, and tenant and employee engagement. This will likely require a combination of elements: breaking down functional silos, enhancing leadership and organizational agility, increasing levels of collaboration and communication, and engaging in transparent and ethical decision-making. Traversing the tightrope effectively in these ways could differentiate organizations from their less successful competitors in the not-too-distant future.